Costs

Costs are the expenses involved in making a product. Firms incur costs by trading.

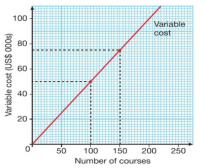

Some costs, called variable costs, cost change with the amount produced. For example, the cost of raw materials rises as more output is made.

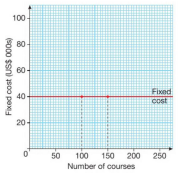

Other costs, called fixed costs, stay the same even if more is produced. Office rent is an example of a fixed cost which remains the same each month even if output rises.

- Variable cost – costs that changes with the level of output

- Fixed Cost – costs that do not vary when output levels change

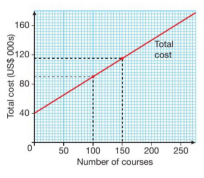

- Total Costs – Fixed cost and variable cost added together.

Total Cost = Fixed costs + Variable costs

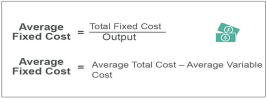

Average Costs

– The average cost of production is the cost of producing a single unit of output.

Total Revenue – money generated from the sale of output. It is price multiplied by quantity.

Profit

Profit = Total revenue – Total cost

Still got a question? Leave a comment

Leave a comment