The Fiscal Policy

A budget is a statement that lays down the government’s plans to spend and raise revenue.

Budget deficit: government expenditure > government revenue

Budget surplus: government revenue > government expenditure

Balanced budget: government revenue = government expenditure

How do governments earn revenue?

- Tax revenue

- Interest payments on government loans to private sector firms and overseas governments.

- Rents from publicly owned buildings + admission charges (eg. museum or national monuments).

- Revenue from government agencies and state-owned enterprises(eg. airports).

- From the sale of state-owned enterprises to the private sector.

The public sector borrowing requirement is the amount of money needed by the government to manage any budget deficit.

The total money borrowed by the public sector over time that has yet to be repaid is called national debt.

Why do governments spend?

1. To influence economic activity:

- C

- I

- G

- (X-M)

2. To reduce market failure:

Expenditure on public goods

Expenditure on subsidies for merit goods

Prevent market failure such as through abuse of monopoly power

3. To promote equality:

As the government provides certain benefits such as pensions to vulnerable groups

4. To pay interest on national debt:

As the loans taken for the public sector borrowing requirement

Why do governments introduce taxes?

- To redistribute income: the government tries to distribute income from the rich to the poor

- To discourage consumption of demerit goods: adding taxes to demerits will increase its prices and reduce consumption

- To raise the costs on firms that impose external costs: as this keeps firms aware of the external costs imposed by them (eg. pollution)

- To discourage the consumption of imported goods: the government aims to protect domestic industries to provide a balance of payment stability.

- To influence economic activity: to influence AD

Principles of taxation

Equity: people or firms should be taxed on their ability to pay (fairness)

Certainty: Easy to understand and calculate

Convenience: Easy to pay

Economy: The cost of collecting tax should be less than the revenue it generates

Flexibility: should be easy to change tax rates with changes in economic

environment (automatic stabilizers)

Efficiency: taxes should not be set such that they will reduce the efficiency of the

market (create a disincentive for example)

Types of taxes

Taxes are either direct or indirect in nature.

Direct taxes – tax on income or wealth.

- Income tax – tax on income/salary.

- Other payroll taxes

- Corporation tax – tax on business profits

- Capital gains tax – tax on profits on sale of assets

- Wealth tax – Taxes on possession of wealth like property tax, inheritance tax etc.

Indirect taxes – tax on consumption. E.g. GST or VAT

Categorizing tax by nature

- Progressive: as income increases rate of taxation increases

- Proportional: no change in rate of tax(flat rate of taxation) for all levels of income

- Regressive: as income increases rate of taxation decreases

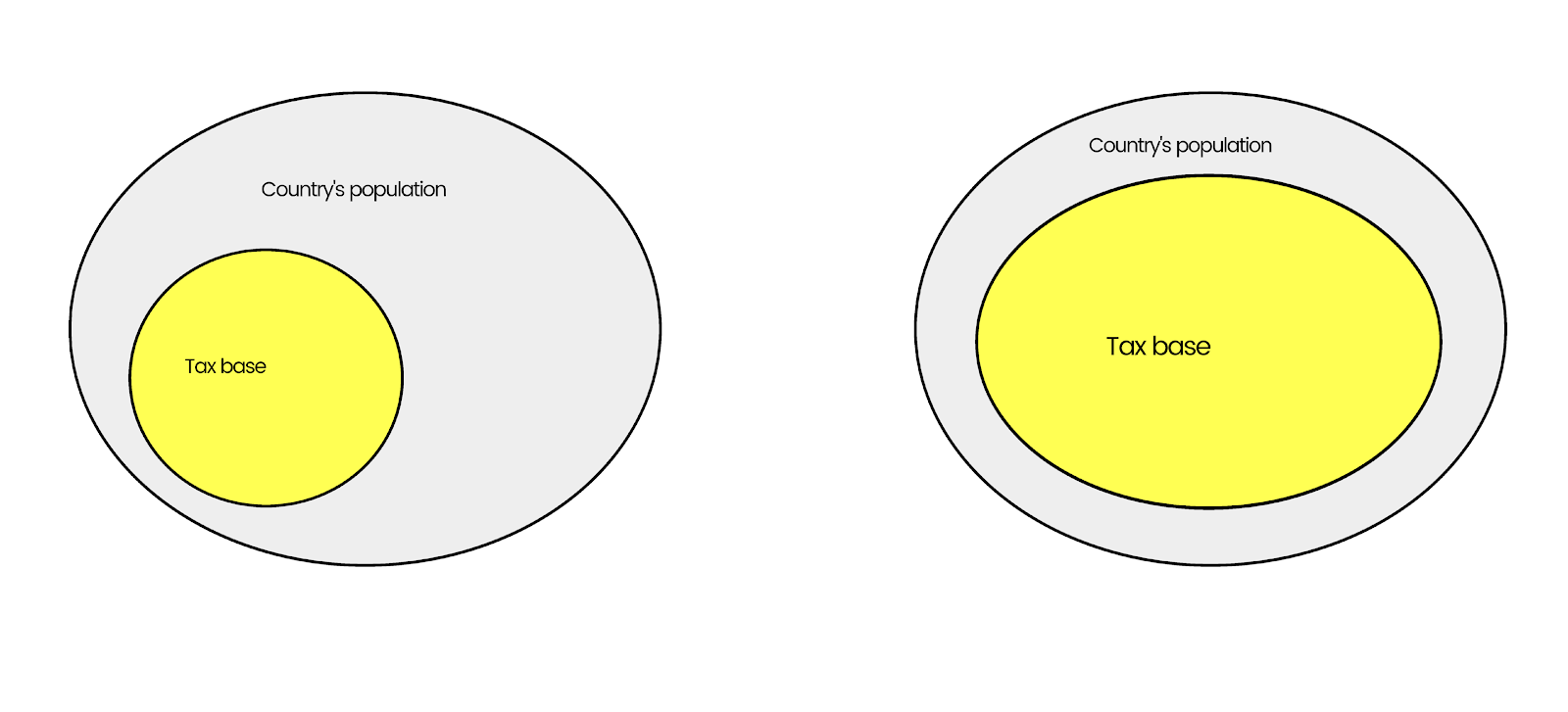

Tax base and tax burden

The more the number of people who can be taxed more the tax base.

More the tax base tax rate can be kept low.

A smaller tax base forces the government to increase tax rates which forces companies to move out of the country or find loopholes to avoid paying tax.

Tax burden: amount of tax paid by people or firms [expressed as a percentage of a country’s GDP]

Impact of direct taxes (or impact of increase in tax)

- High taxes might discourage effort, enterprise, and saving.

- High-income tax might prevent people from working overtime, taking promotions, and prevent people from entering the labor force.

- High-income tax may prevent firms from expanding and investing in new markets.

- High tax rates might encourage people with fixed financial commitments to work harder.

- A high tax on saving might deter people from saving but encourage target savers to save more.

- Direct taxes act as automatic stabilizers.

Impact of indirect taxes

- As indirect taxes are regressive in nature, an increase will disproportionately burden poor people

- An increase in indirect taxes raises prices thereby leading to inflation

- They are less of a disincentive to work and enterprise in comparison to direct tax increases.

- They are harder to evade.

- They are easier and cheaper to collect.

- They provide choice to the buyer as buyers will pay for only those items purchased.

- Indirect taxes are a good option to collect taxes where there is a large informal economy and low literacy rates.

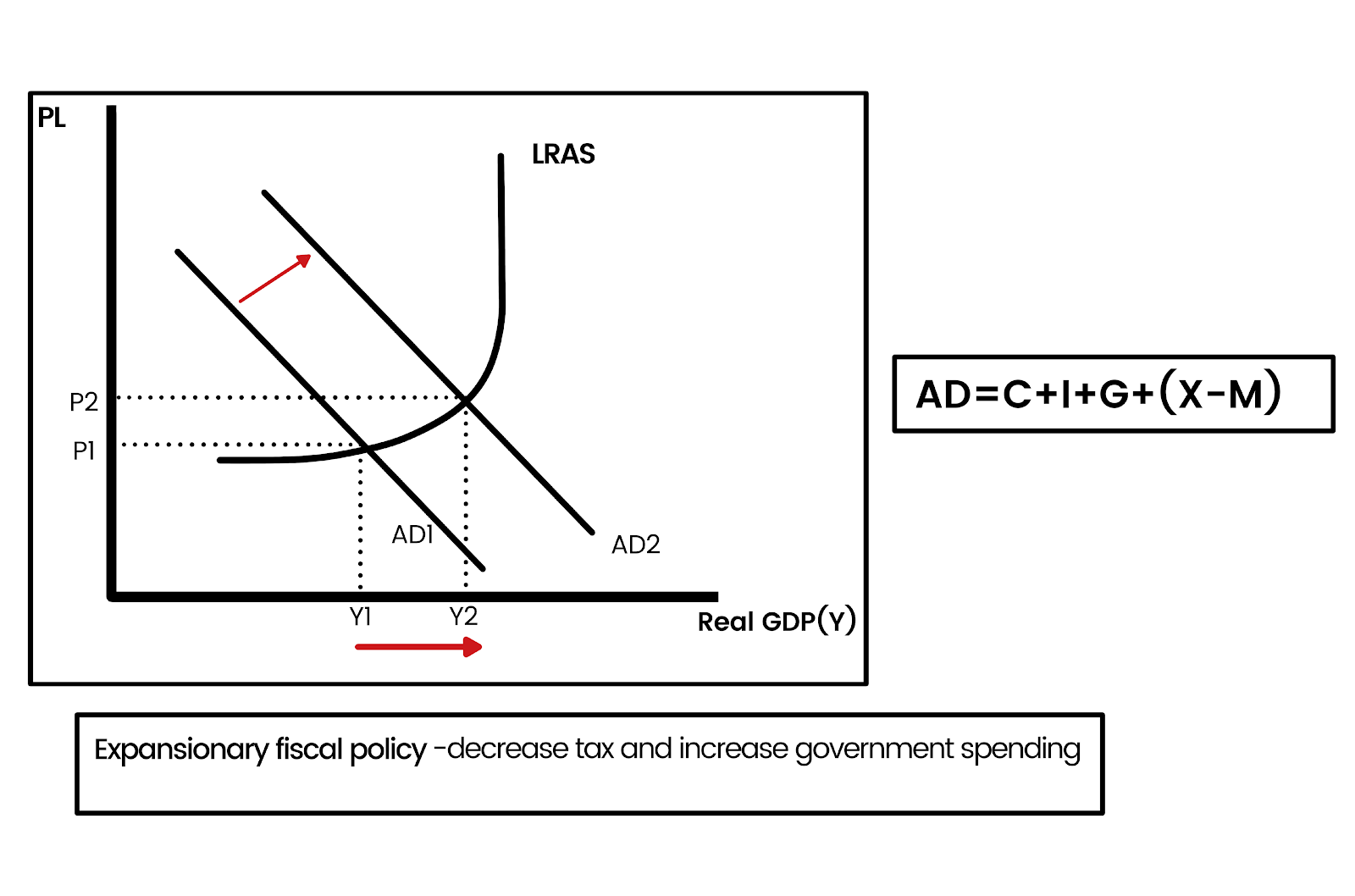

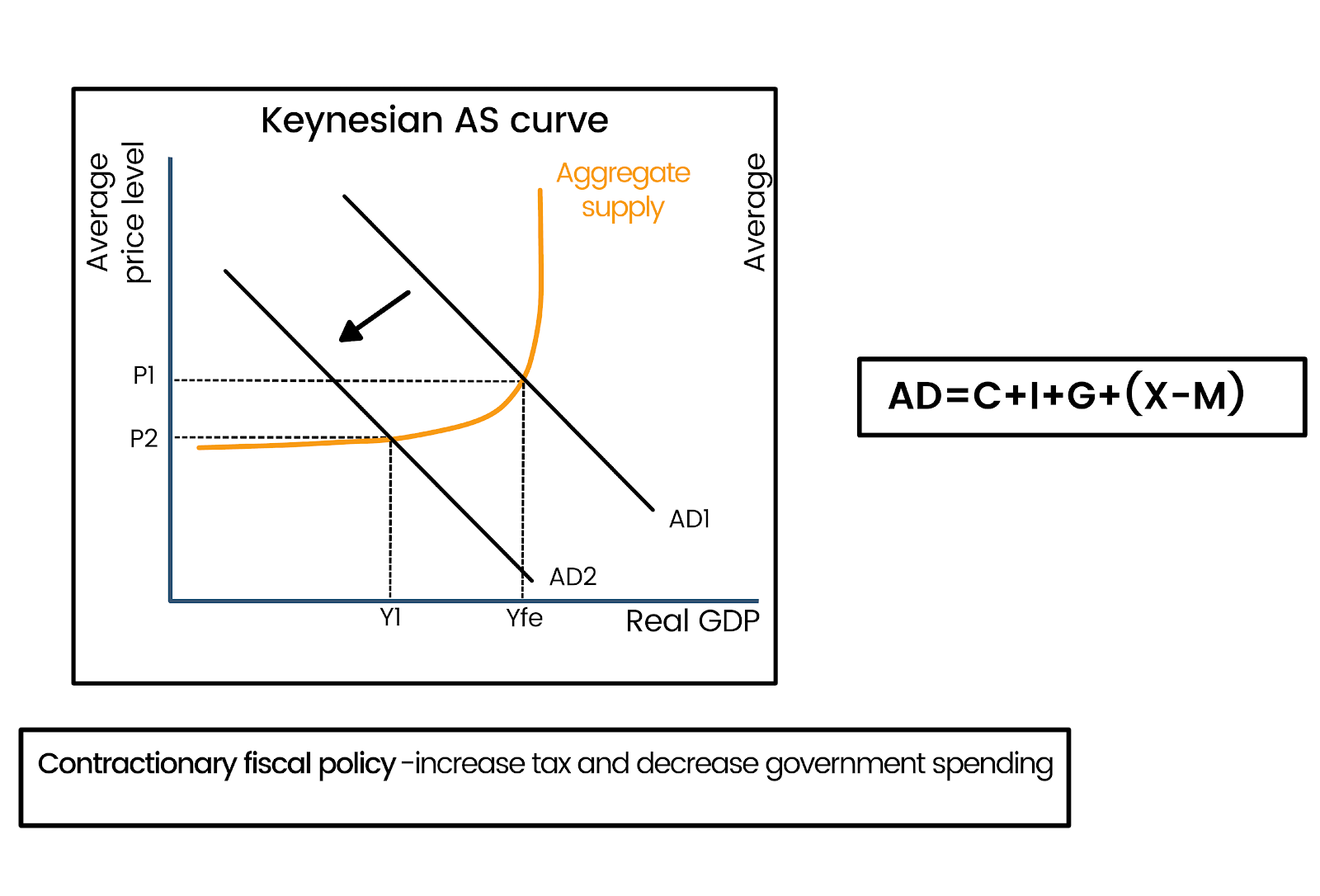

What is fiscal policy?

Fiscal policy involves varying the overall level of public expenditure and/or taxation in an economy to manage aggregate demand and influence the level of economic activity.

Expansionary fiscal policy is when the government aims to increase aggregate demand in an economy to boost employment and output by increasing its expenditure and/or reducing taxation.

Contractionary fiscal policy is when the government aims to reduce pressure on prices in an economy by cutting aggregate demand through a reduction in public expenditure and/or by raising total taxation.

Problems with fiscal policy

- It is cumbersome to use

- Riddled with time lags

- Could lead to overheating (rapid inflation of prices)

- Increase in public expenditure crowds out private spending

- Increasing taxes on income and profits can reduce incentive to and work and enterprise.

An expansionary fiscal policy creates expectations of inflation.

Still got a question? Leave a comment

Leave a comment